Trump’s approval is bad enough. No need to exaggerate.

It’s the one year mark of Trump’s second term and everyone is posting year in review pieces. Here is mine.

The chart shows how all presidents in the polling era have varied in approval over their entire terms, plus year 1 of Trump 2.0. The boxes cover the middle 50% of all polls, and the “whiskers” extend out to their all time highs and lows of approval in Gallup polls. The bar in the box is the median poll, the 50th percentile. I stick to Gallup for consistency over time and for their unmatched historical depth.

What jumps out is the approval ratings of the last four presidents have varied considerably less than those of their predecessors. Trump 1.0 has the least variation (smallest standard deviation) of any of the other 14 presidents, with 2.0 the second smallest, so far. Both Obama and Biden varied a little more, but considerably less than either Bushes, Clinton, or Reagan. Trump’s median in 1.0 ties with Truman for the lowest median approval, 39%. So far, Trump 2.0 is the 3rd lowest, at 40.5%. (Truman, by the way, set the record for all time low at 22%. Trump hasn’t come close, with a low of 33%, so far.)

This shrinkage of variation in approval is one consequence of polarization, leading the out-party since George W. Bush’s 2nd term to consistently give approval ratings below 10%, while the in-party gives high approval, typically in the 80s, no matter what. The poor independents are left to shift the balance a bit between two largely unmovable partisan camps. V.O. Key famously said voters were “a rational god of vengeance and reward”, but that breaks down when one side will never reward good performance and the other will never condemn bad outcomes. Trump may never approach the lows of Truman, Nixon, Carter or both Bushes, all of whom had low points in the 20s. But he will never approach the highs of Obama, Clinton or Reagan either.

Here is a more conventional look at approval of each of the elected presidents from the polling era. The trends here are smoothed trend estimates. Gallup now polls approval only once a month, so Trump 2.0 is not smoothed, just the raw polls. Also, Gallup hasn’t released the January results, so December is the most recent reading.

Trump 2.0 has run a little better than 1.0 in Gallup’s data. The December point at 36% is a bit of an outlier. The major polling averages put Trump’s approval between 40% and 42% as of Jan. 20, 2026.

An alternate view breaks out each president for readability. Here I’m showing raw poll results with no smoothing.

Here is my polling average for all Trump polls in 2025. My trend estimate is 41.4% approval. For comparison, FiftyPlusOne.news has it at 40.0%, SilverBulletin is 42.0%, NYTimes is 42.0% and RealClearPolitics is 42.4%.

You will note dips below the general downward trend in April after the tariff announcement, then a little recovery after backing off those original “liberation day” tariffs. Then the downward trend returns, until another dip during and after the government shutdown in October and November. A bit of a rise in early December after which the general downtrend returns. This is steady, nearly linear, decline with a couple of short-term wiggles.

I have a beef with headlines that shout “Trump at all time low” or “Approval cratering.” Those either cherry pick particularly low polls, or exaggerate small departures from the general downward trend. Trump’s approval is bad enough. Historically low for other presidents at the end of one year. But the message I read in this trend is a steady decline in approval for an unpopular president, signaling a challenging midterm, and with no sustained upturn in the last 12 months. No need to exaggerate the problems this poses for the White House or Republicans generally.

After a year in office, opinions about Donald Trump are a bit more complicated than merely “approve” or “disapprove.” Those who disapprove find almost nothing to like, but those who approve are likely to express mixed feelings, reporting things they dislike even if on balance they approve of the job he is doing as president.

For over a year my Marquette Law School Poll national surveys have asked a pair of open-ended questions in each poll:

What do you like about Donald Trump?

and

What do you dislike about Donald Trump?

Respondents can write as much or as little as they wish. The record is over 900 words. Much more common than full op-ed length answers are “everything” and “nothing”, in either order.

The pure-admiration and pure-hate answers can be short or long, but each give insights into how people think about Trump. Still, a substantial number of people have mixed feelings. Among Trump supporters it is common to see approval of his actions or policies coupled with disliking “how he talks” or “how he deals with people” or “the Epstein files.” It is less common to find those who disapprove of Trump seeing anything to like. If the substance of the dislikes goes to his policies then we see fewer finding positive things as well.

In a year of polling these questions, we have seen a notable trend. Respondents with mixed feelings, giving both likes and dislikes, have declined from 51% to 44%, while those who don’t like anything have climbed from 35% to 42%. And the true Trump fans, who only find something to like and nothing to dislike, have slightly declined from a high of 14% to 10%.

This gives a different perspective on Trump’s approval ratings, which have held between 40% and 42% in the current polling averages, down from the start of the second term but hardly “collapsing” as some suggest.

Among those who disapprove, few exhibit mixed feelings in the open-ended responses. They see nothing positive and vary primarily in the length and detail of their vitriol. The past year has grown this group of people, irreconcilably opposed to Trump.

We often think Trump’s base is rock solid. Approval among Republicans remains around 85% a year into Trump 2.0. But the open-ended responses suggest a more complicated story. Among his supporters, those who approve of the job he is doing, the substantial majority have mixed feelings in the open-ended answers. This does not forecast a collapse of his approval, but it does remind us that the caricature of his base as mindlessly in love is not accurate. So far, they like more than they dislike. But it is not because they are blind to the president’s shortcomings.

While a substantial number of members of the House of Representatives are retiring, don’t expect these retirements to produce many flipped seats or shifts in the ideological makeup of either party.

As of January 13, 47 members of the House have announced their retirement, 21 Democrats and 26 Republicans. (I’m not counting resignations by Majorie Taylor Greene and Mikie Sherrill whose seats will be filled with special elections this year.)

The retirement rate has been running a bit ahead of recent cycles as of this date, which were 42, 34, 41, and 40 from 2018 to 2024. Still, I don’t think we are seeing extraordinarily high levels of retirements, as some commentary suggests. In the end those previous four cycles produced totals of 52, 36, 49 and 45 retirements, suggesting we may end up in the mid-to-upper 50s this year. Past retirements are from Ballotpedia.org.

The main point I want to make here is that the retirements are spread pretty widely throughout both Republican and Democratic caucuses by ideology and 2024 vote margin. The solid dots are retiring members. These are not endangered incumbents who barely scraped by in 2024, nor are they ideological outliers relative to their caucuses.

The figure shows all House members by vote margin and by left-right ideology, using Nokken-Poole dimension 1 ideology scores from VoteView.com. These scores are based on roll call votes by the members. Nokken-Poole is a variant of the widely used Nominate scores. Nokken-Poole scores range from -0.848 for the most liberal member to 0.986 for the most conservative member. Vote margin is the percentage for the Republican candidate minus the percentage for the Democrat, so negative margins are Democratic wins and positive ones are Republican victories.

Among Republicans, the median 2024 vote margin is 28.2 percentage points, and the median for retiring Republicans is 26.1 points. On ideology, the median Nokken-Poole score is 0.542 (higher scores are more conservative.) Among retiring Republicans the median is 0.581

Democratic retirees have somewhat larger vote margins, -36.8 percentage points, than their caucus as a whole, -27.0 points. On ideology, the retiring Democrats are also more liberal, -0.461, than the full Democratic caucus, -0.394. These are modest differences, however, and the figure makes clear retirements are well scattered throughout both caucuses.

The upshot of this distribution of retirements is that it does not open up many opportunities for turnover as most retirees enjoyed reasonably secure margins in 2024. Nor are retirements likely to significantly shift the ideological balance in the House given that retirees are ideologically pretty representative of their caucuses. While open races are less predictable than incumbent ones, the strong partisan lean of most of these districts means we should expect no more than a handful of these seats to potentially flip.

DCCC and NRCC target districts

Both the Democratic Congressional Campaign Committe (DCCC) and the National Republican Congressional Committee (NRCC) have released lists of districts being targeted as pick up opportunities. Compare this figure with the retirements above. The targeted districts are, as you would expect, far more concentrated in races that were narrowly decided in 2024. (These lists were released by the NRCC on March 17, and by the DCCC on April 8. They do not include changes or additions after some states redistricted in 2025. These are the members’ districts in the 119th congress.)

Republicans on the DCCC list have a median vote margin of 6.8 percentage points, much closer than the caucus median of 28.2 points. They are also less conservative, 0.384, than the full caucus, 0.542.

Democrats on the NRCC list also had much closer 2024 races, with a median of -3.2 percentage points compared to -27.0 for the full caucus. These Democrats are also less liberal than the caucus, with a median Nokken-Poole score of -0.221 compared to the caucus median of -0.394.

If you are looking for change in the House, look at the districts each of the parties are focusing on. They have a much greater chance of flipping than the seats of retiring members, and would be more likely to remove relatively moderate members of either party. The latter fact will also contribute to polarization in the House. Rather than target ideologically extreme members of the opposition party, both Democats and Republicans target close races, which also happen to be where the most relatively moderate members are.

Wisconsin’s Supreme Court elections were once low-key, low-turnout April affairs. Not so much any more. In 2023 total spending on the court race reached $50 million. Two years later, in 2025, total spending doubled that, passing $100 million. The big spending reflects the stakes in a shifting majority on the court. In the 2019-20 term, conservatives held a 5-2 majority. In 2020 liberals narrowed the conservative majority to 4-3. After the 2023 election it became a 4-3 liberal majority, which was maintained in 2025. With a retiring conservative justice, the 2026 election can either hold the 4-3 liberal majority or increase it to 5-2 for the 2026-27 term. (The seven justices are elected to 10 year terms.)

This recent shift contrasts with consistent conservative majorities from 1995 until the recent shifts. The figure shows the results of court elections since 1995. From 1995 through 2003 conservatives won 5 elections to 2 for liberals. From 2005 to 2013 conservatives again won 5 elections to 2 for liberals. But since 2015 liberals have won 5 seats to 3 for conservatives.

Since the 1990s Wisconsin Supreme Court elections have become far more partisan with voting patterns coming to be strongly linked to partisan elections and with the parties endorsing and financially supporting candidates in the formally non-partisan court races.

The next figure shows this changing partisan structure to court voting. As an example, I use Justice Ann Walsh Bradley, who won in 1995 and 2015 before retiring in 2025. (In 2005 she ran unopposed.) In 1995, there was a moderate correlation, .45, between how counties voted for the court race and how they voted in the previous presidential race. But by 2015, the correlation between Bradley’s vote and the 2012 presidential vote had risen to .78. In 2025 when Bradley retired, the correlation for liberal Susan Crawford with the 2024 presidential vote was an astonishing .99. This reflects the surge in party polarization in Wisconsin and the emergence of court races more tightly tied to partisan divisions.

This increase in partisan voting structure is not a sudden phenomena, but one which has grown steadily since the 1990s. In the 1970s and 1980s there was little partisan structure to court elections. Indeed, in 1978 the correlation was nil, .002. This rose sporadically in the 1990s, then grew steadily since 2007 to the current astonishingly high .99 of 2025.

This extremely high correlation doesn’t mean outcomes are locked in. Justice Brian Hagedorn, a conservative, won in 2019 by less than a 1 percentage point margin, with a correlation of .92 with the 2016 outcome, while Justice Rebecca Dallet, a liberal, won the year before with a 10 point margin and a correlation of .89 with the same 2016 presidential race. If all counties shift their votes up or down by the same amount, the correlation remains high though the outcome can shift, as in these two cases. Correlation tells us about the structure of the votes but not where the majority necessarily falls. What we have now is that the most Republican counties are now virtually certain to also be the most conservative in their court votes and the most Democratic counties the most liberal. That wasn’t the case before the 1990s when knowing a county’s presidential vote told us very little about their court vote.

The April 2026 election is likely to reflect this strong partisan structure of voting, though we can’t yet say if the net election forces will shift in the liberal or conservative direction.

The geography of the court vote has shifted dramatically over 30 years. In 1995, liberal Justice Bradley won with 55% of the vote. In 2025, liberal Justice Crawford replaced the retiring Bradley with a nearly identical 55% of the vote. But the sources of these two victories was dramatically different. In 1995, Bradley was strongly supported in the north, north-central, and southwestern parts of the state. Notably her vote was significantly less in Brown, Dane and Milwaukee counties. In 2025, Crawford lost badly in the north, north-central and most of the southeast, while she ran up large margins in Dane and Milwaukee, much more than Bradley’s 1995 totals in those counties. She also ran a little ahead in Brown, a county Bradley had lost badly in 1995. The maps shows how dramatically the geography of the vote has shifted even with identical vote margins in the two races.

With so much of the state shifting from blue to red, how is it that the vote margin is unchanged? Democratic gains have been large and come in counties with large populations. Republican gains are widespread but mostly in less populous counties. In large Republican leaning counties, Waukesha, for example, the conservative majority has increased but only slightly, with a larger increase in Washington, but a slight decrease in Ozaukee. Republicans have gained in Marathon, but the conservative margin is only moderate.In contrast, Dane has gone from pretty liberal to overwhelmingly liberal, and Milwaukee which was quite competitive has also become very liberal in its court vote. These shifts also highlight the greater geographic polarization in the 2020s compared to the 1990s, while not shifting the statewide balance at all.

Public opinion

Since 2023 the Wisconsin Supreme Court has held a consistent net approval rating, though about 15% say they don’t have an opinion. Court approval slightly improved during and after the 2025 court election, declining slightly in October.

As of October, the candidates for the court in 2026 were little known to the public. This is not unusual in court elections and especially so with no incumbent. The Marquette Law School poll in October asked registered voters if they had a clear idea what the candidates stand for. For both candidates, 69% said they hadn’t heard enough, and only 10% or 11% said they did have a clear idea. With less than 3 months left before the April election, the campaigns have a lot of messaging to do.

Voters have a strong preference that candidates for the court discuss issues so voters know what they stand for, 83%, while only 17% say candidates should avoid discussing issues so as to not appear to have prejudged issues. On this, partisans and independents are in agreement.

The balance of the court

With the current balance of the court, and the justices coming up for election in the next 10 years, the liberal majority is assured until at least 2028. Should the liberal candidate win in 2026 the majority will remain in liberal hands until at least 2030 (absent an unscheduled vacancy occuring.)

After more than two decades of conservative majorities, the liberal victories in five of the last eight court elections has altered the balance, and created the prospect for continued majorities well into the 2020s or beyond.

The shifting balance of the court since 2019 is shown in the table below.

And for those who want way more detail (you know who you are), here are all Wisconsin Supreme Court elections since 1976. My ideological classification of justices may be debatable in some cases prior to 2000. In those less partisan times ideology played less of a role and moderate justices may be mislabled. The distinctions since 1995 are much more clear, though note that Hagedorn was elected as a conservative candidate but does not align strongly with either the liberal or conservative wings of the court in his decisions, siding with conservatives a little more than half the time in some terms and a little more than half with liberals in other terms. See the excellent SCOWstats.com for detailed analysis of court alignments since 1918.

On January 8, the House passed a bill to extend enhanced Affordable Care Act subsidies for three years. Despite leadership opposition, 17 Republicans voted for the extension, a notable break with the party majority. An additional 5 Republicans did not vote. The bill’s prospects in the Senate are unclear as negotiations in that chamber continue.

Those Republicans voting for the bill had closer elections in 2024, and are less conservative than the GOP caucus as a whole. The Republicans who did not vote had larger 2024 vote margins and are somewhat more conservative than those who voted for the bill. The figure shows all members of the House. Those voting Yea are solid circles, Nays are open circles and non-voters are solid triangles. All Democrats voted for the bill.

For Wisconsin readers (and The Downballot fans like me) I’ve highlighted Derrick Van Orden, WI03, the only Republican from Wisconsin voting for passage. Van Orden won by the smallest margin (2.7 percentage points) of Republican House members in the state in 2024, and is a target for Democrats’ efforts to win the House in 2026. As with others voting to extend the tax credits, Van Orden is less conservative than the GOP caucus and had a close 2024 race.

The table shows all Republicans who voted for the tax credit extension, and those who did not vote.

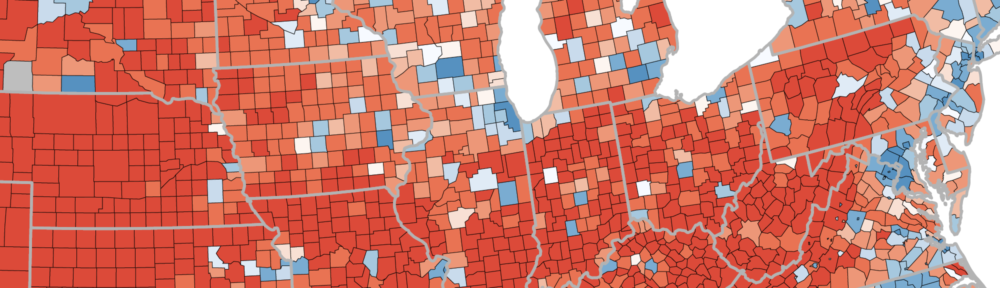

The geography of GOP defectors is interesting, especially three from New York (all in the south), three from Pennsylvania (all in the east) and three from Ohio (northeast and central). Also notable is the lack of defections through most of the south and west. (Credit the map to VoteView.com) (In the map OH15 looks like 2 districts because it has a very narrow waist connecting the east and west lobes of the district.)

Seventeen defectors hardly amounts to outright rebellion, though with the extraordinarily narrow GOP majority it easily swings the outcome of the roll call. These members have good reason to be concerned about their reelection prospects in November, and do not come from the most conservative wing of their party. Whether any suffer consequences from the leadership or the White House remains to be seen. When party unity has been so strong through 2025, this departure signals that members have concerns for voter reaction that can overcome party loyalty on some issues.

We also saw five Senate Republicans defect to advance a war powers resolution on January 8. And 35 Republicans voted to override Trump’s veto of a Colorado water project, with 24 voting to override a veto concerning tribal lands in Florida. While limited, this is more pushback from congressional Republicans than the Trump administration saw in the first year back in power.

Time for a look back at the news of 2025 and what the public paid attention to and what it largely ignored. The year has not lacked for news, especially political news as Donald Trump expanded his authority through executive orders, followed by litigation over those orders.

My Marquette Law School Poll asks how much people have heard or read about recent events in the news in each poll:

Here are some recent topics in the news. How much have you heard or read about each of these?

Polls are conducted every other month, six times a year. This is not a comprehensive review of news events but provides a look at how much attention the public gave to a wide variety of mostly political news. Topics are picked from recent events that have received significant coverage and raise important political issues, with more emphasis on news stories published within a few weeks of each poll’s field dates.

Figure 1 shows the 32 topics asked about over the year.

The top topic of the year, by a substantial margin, is tariffs. The May survey came a month after Trump’s “Liberation Day” announcement of tariffs on April 2 and the subsequent changes made in rates and implementation dates. Fully 81% of U.S. adults said they had heard or read a lot about the tariffs.

The second most attention went to Trump’s plans for deportation of immigrants in the U.S. illegally, with 70% hearing a lot about this in the first month of the administration. Subsequent items concerning immigration issues varied in visibility, with the mistaken deportation of a man, Kilmar Abrego Garcia, who was sent to El Salvador in March ranking as the 7th most followed event, with 63% hearing a lot. When Garcia was returned to the U.S. in June, only 37% heard a lot about that, ranking 25th of 32 news items.

Cuts to the federal workforce ranked 3rd most followed story, with 67% hearing a lot as of May. Rounding out the top five news items were the war between Israel and Iran in June and the contentious meeting between Trump and Ukraine President Volodymyr Zelenskyy on February 28th in the Oval Office. U.S. airstrikes on nuclear facilities in Iran ranked 6th.

At the bottom of the chart are Trump’s attempts to remove a member of the Federal Reserve Board and the firing of the director of the Centers for Disease Control, followed closely by 30% and 29% respectively.

If you follow politics enough to be reading this post you will probably to shocked that attention to the November elections for governor in New Jersey and Virginia ranks 31st of 32 events, with only 28% hearing a lot about this. For us political junkies, it is a reminder that much of the public doesn’t follow politics closely, and especially not elections in states other than their own.

The honor of being the least followed of the 32 stories is Trump’s extended diplomatic trip to Asia in late October, during the shutdown of the federal government, with only 24% who paid a lot of attention to that trip.

Attention to news by party

Figure 2 shows attention to these news topics by party. A higher percentage of Democrats than Republicans say they have read or heard a lot about most of the news events covered during 2025. By comparison to either party, independents are considerably less likely to have followed news across every item.

Highly visible events receive more attention across all partisan lines while more obscure events are also followed less by each party group. The correlation of attention for Democrats and Republicans is .78. Independent attention correlates with Democratic attention at .91, and with Republican attention at .85. In short, news tends to penetrate each partisan group in similar ways though with generally lower attention from Republicans and especially independents.

Republican vs Democratic attention to news

Figure 3 shows the attention gap between Republicans and Democrats across the 32 topics, arranged by size of the difference between Republican and Democratic attention. For the news items we asked about, Democrats say they have heard or read more than do Republicans for 24 items, Republicans more for 5 items and the parties are tied for 3 items.

It is notable that the items with greater attention from Republicans are closely tied to Trump. Attention to his inaugural address shows the largest Republican advantage over Democrats in attention, 27-percentage points, followed by Trump’s speech to a joint session of Congress (don’t call it a State of the Union address) with an 11-point GOP lead in attention. Other topics with a Republican advantage closely concern Trump–the cease-fire agreement between Israel and Hamas and the U.S. airstrikes on Iranian nuclear facilities.

At the opposite end of the partisan attention gap, Democrats paid much more attention to the “No Kings” protests in October, by 23-points, and to a measles outbreak in Texas and New Mexico in the winter by 20-points. Democrats also paid substantially more attention than Republicans to the firing of the CDC director and reductions in the federal workforce.

Perhaps surprisingly, Democrats paid considerably more attention in September to the potential release of the Jeffrey Epstein files than did Republicans, by 16-points. (This does not cover the actual release of the files in December, after our final poll of 2025 in November.) Coverage of this issue has emphasized pressure from Republicans and MAGA activists for the release, though Democrats also supported the law to require the files to be made public.

This invites the question of whether Democrats simply pay more attention to politics than do Republicans.

In fact, attention to politics is virtually identical for Republicans and Democrats, while independents are much less attentive in general. We ask

Some people seem to follow what’s going on in politics most of the time, whether there’s an election going on or not. Others aren’t that interested. How often do you follow what’s going on in politics…?

Forty-nine percent of Democrats say they follow politics most of the time, as do 48% of Republicans, a trivial difference. In contrast, only 26% of independents say they follow politics most of the time. The lower attention from independents is reflected in their notably lower levels of attention to news events, but this can’t account for Republican and Democratic differences across news items. Table 1 shows attention to politics by partisanship in 2025 surveys.

One plausible explanation is that partisans follow different news sources, and those sources give different emphasis to specific news events. I don’t have data on the actual content of various news sources, but in my data there are only small (typically 3-4 point differences) in awareness of news events between Republicans who follow only conservative news sources and those who follow a mix of conservative and liberal sources, and a similarly small difference for Democrats who follow only liberal sources versus a mix of liberal and conservative sources. This casts some doubt on the idea that it is differences in content that drives differential awareness, and suggests that partisanship has more to do with what news people pay attention to, and remember. More on this in a future post.

The data tables

For those who want to see the numbers in detail here you go. Table 2 shows those who heard or read a lot, a little and nothing at all for each news event. While there is some variation, the most prominent news items have high “heard a lot” and low “nothing at all”, and the less prominent items reverse this.

Table 3 shows high attention to news by party identification.

The cost of living, or “affordability”, is at the top of public concerns likely to shape the 2026 elections. Let’s look back over the last decade for some perspective.

For the past 10 years my Marquette Law School Poll has asked Wisconsin registered voters about their family’s financial situation:

Thinking about your family’s financial situation, would you say you are living comfortably, just getting by, or struggling to make ends meet?

The percentage saying they were living comfortably rose steadily during the first Trump administration, from around 50% in 2016 to over 60% by 2020. But as inflation rose in 2021 the trend reversed, falling to 44% near the end of the Biden administration in late 2024. In the first year of the second Trump term the percentage living comfortably has turned up modestly, standing at 50% as of October.

Those who say they are just getting by reverse the pattern for those living comfortably, declining from 2016-20, rising from 2021-24, with a slight downturn in 2025. Those struggling also move in rough parallel with those just getting by.

The decline in financial well-being during the Biden administration goes a long way to explaining Biden’s low approval rating during the last three years of his administration and Trump’s ability to win Wisconsin in 2024 by 0.9 percentage points, after having lost the state by 0.6 points in 2020.

The upturn in financial situation in 2025 contrasts with continued worries about inflation and the cost of living, which was the most cited problem in the October Marquette poll, at 27%, with an additional 9% citing the economy as most important. These concerns are substantial across the usual partisan lines: 23% of Republicans rank inflation as most important, as do 27% of independents and 32% of Democrats. Only Republicans rank another issue higher, immigration, at 31%.

What lies behind the changing sense of financial security or insecurity over the past decade? Partisanship plays a big role, as does income.

Family finances by party identification

The upturn in sense of living comfortably in 2025 is entirely due to Republicans who turned sharply more positive with the change of administration in January. By the end of the Biden administration only about 34% of Republicans said they were living comfortably, but by October this had soared to 63%.

In contrast, independents living comfortably declined throughout the Biden administration and show no upturn in 2025. Democrats viewed their financial situation as stable through the Biden years with a substantial downturn in 2025.

There is no evidence these changes in perceived financial situation reflect real fluctuations in income. In 2024, 37% of Republicans reported family incomes over $100,000, and 37% had that income in 2025. For independents, 28% had this level of income in both 2024 and 2025. Slightly more Democrats had incomes over $100,000 in 2025, 34%, than the 32% in 2024.

Family finances by income

This powerful effect of partisanship does not mean money doesn’t matter. Those living comfortably rises with income while those struggling goes down as income rises. More important is the changing sense of well-being over time and especially during the Biden years. Across each income level the percentage living comfortably fell during Biden’s term after rising during Trump’s first term. Those struggling declined or was flat during Trump’s first term but rose under Biden, especially for lower income families, though also for those of middle-income. For the high income group a decline in living comfortably translated into a rise in the feeling of just getting by. In 2025 all income groups show at least a small increase in sense of living comfortably and a downturn in those saying they are struggling.

Family finances by party ID and by income

We can disentangle the income and partisan effects a bit by looking at both simultaneously. Republicans, regardless of income, showed declining financial well-being throughout Biden’s term and have shown an improved outlook in 2025. (The data here are aggregated by year to provide enough cases to reliably estimate both partisan and income effects simultaneously.)

Both low- and high-income independents had declining finances in 2021-24 and continued down in 2025. Middle-income independents seem a bit better off in 2024 and 2025 than earlier in Biden’s term.

Low- and high-income Democrats held stable in their sense of family finances under Biden, with both dropping off a bit in 2025 under Trump. This contrasts with middle-income Democrats who felt increasingly worse off under Biden and are continuing down under Trump.

Not to be missed in all these details is that among Republicans and independents every income group felt their financial situation was better during Trump’s first term than during Biden’s. Democrats were more stable during the Biden years, with the important exception of middle-income Democrats who felt increasingly worse off.

Finances, party and the vote

The sage said, “it’s the economy, stupid” and this seems to hold up today as it did in the 1990s. If not the only thing that matters, these shifts in financial security from 2021-24 surely go a long way to pointing us to crucial groups who found themselves feeling worse off in 2024 than in 2020. This was especially true for middle-income people who reported being less secure regardless of party by 2024. For Republicans this reinforced their partisan inclinations while for Democrats greater insecurity is associated with a modest increase in votes for Trump, and likely reduced turnout: among Democrats living comfortably, 96% said they were certain to vote in 2024, while among those struggling 86% said the same. Turnout increased slightly for struggling Republicans vs comfortable ones, while turnout was lower for struggling independents than those living comfortably.

Voting for Trump was higher in 2024 for those struggling compared to the comfortable across parties, with modest differences among Republicans and Democrats but a large 40-point increase for Trump among struggling independents vs. comfortable ones.

The lesson for 2026 and beyond: “it’s the economy, stupid”.

Contrasting takes on religion and the young. There have been a number of stories like this Washington Post piece with vivid and interesting examples of 20-somethings embracing religion. (Link should allow door through the paywall.) https://wapo.st/3KltFEh

The newspaper stories aren’t misleading about specific cases. Obviously individual local churches may be growing and flourishing even as the national picture is one of stability or decline. But it is a reminder that there is pressure to generalize from specific instances to broad generalizations. Caution and perspective are helpful.

The president’s party almost always suffers in the House

Midterms are less than a year away so it’s time to look back at the record.

In the House, the president’s party has lost seats in all but four midterms since 1862, and one of those, 1902, was a year the House expanded so the Republican gains fell short of Democratic gains that year. After 1934 it wasn’t until 1998 that the president’s party gained seats, then the rare event repeated in 2002. Not since.

This regularity over 160 years is hard to attribute to the circumstances of the moment. Likewise the hope that “this year will be different” has been a forlorn one. The size of the seat loss, on the other hand, has varied considerably and is correlated with presidential approval (Clinton in 1998 and Bush in 2002 were unusually popular, as was Roosevelt in 1934) and the state of the economy. Popular presidents lose fewer seats, unpopular ones more. Good times go with smaller losses, bad times with greater losses.

In 2026 we will have the unprecedented circumstance of a large number of mid-decade redistricting decisions as the parties battle to see who can gerrymander the most seats to their advantage. That landscape is still being painted.

In the Senate the pattern of losses are much less dependable than in the House. The president’s party usually loses seats, and the gains have been small since the 1940s. The vagaries of which seats are up and how many for each party adds uncertainty to the Senate picture. And, of course, prior to 1913 the Senate was not elected by popular vote.

In the House, the second midterm for a president produces barely grater losses than the first midterm (an average of 28.9 in the second, versus 24.9 in the first.) There isn’t a “six-year itch” on the House side. The Senate has been a different matter, with second midterm losses averaging 6 seats rather than 2 in the first midterm (since 1946.) One plausible explanation for the Senate is that the 6th year is the reelection of a Senate class elected with the president for his first term. To the extent a winning first term president brings along some partisan companions, they run without his coattails 6 years later. The table shows the seat changes and the averages since 1946.

Next year there will be inevitable discussion of whether 2026 is Trump’s second midterm. Obviously it is in one sense. But for the Senate, this will be the class elected with Joe Biden in 2020, not the class elected with Trump in 2016. This group had mild pro-Democratic national forces either helping or hurting them in 2020. Given this difference in the election cycle, the average 6 seat loss may not be as good a representation of expectations for Senate seats in 2026.

They say there are no second acts in politics. In Wisconsin that has been the case for the last 27 years, at least when it comes to statewide contests for governor and U.S. Senate. Mandela Barnes’ entry in the 2026 governor’s race will attempt to break the dismal recent record.

Consider the examples of Tom Barrett (lost governor’s races in 2010 and 2012), Tim Michels (lost Senate race in 2004 and lost governor’s race in 2022), Russ Feingold (lost Senate races in 2010 and 2016), Eric Hovde (lost GOP primary for Senate in 2012, lost Senate race in 2024), and Mark Neumann (lost Senate race in 1998, lost GOP primary for governor in 2010 and lost GOP primary for Senate in 2012). Even Tommy Thompson, who won four races for governor, fell short 14 years later in his 2012 bid for the Senate. You have to go back to the 1970s to find a successful second act in Wisconsin statewide elections.

What does this record say about Barnes’ position in the 2026 race for governor? There are some advantages that are important. He will likely start out as the best known candidate in a field of some 7 or 8 candidates. In my Marquette Law School Poll of Wisconsin, Oct. 15-22, the three best known Democrats had name identification ranging from 22% (Hong) to 25% (Rodriguez) to 26% (Crowley), with the rest in the teens. Barnes was not included as he had not entered the race. At the end of his 2022 Senate race, Barnes had a name ID of 85%, though when he started that race as the sitting Lt. Governor his ID rate was 37% in Feb. 2022. There is falloff in ID between races. Barrett finished his 2010 governor’s race with 84% name recognition, which fell to 61% in Jan. 2012 at the start of the recall election. Feingold fell from 95% in 2010 to 75% in Jan. 2016.

In two recent polls that included his name (though unannounced at the time) Barnes was ahead in the Democratic primary field with 16% support in a Sept. 28-30 poll sponsored by Platform Communications and ahead with 21% in a TIPP poll conducted Nov. 17-21. In both polls all other candidates were below 10%, with a third to half of voters undecided. Those polls didn’t measure name recognition.

Barnes also has the advantage of having raised substantial money in his 2022 Senate bid, giving him a donor list to tap that none of the other candidates have.

Those are positive elements for Barnes and each gives him an initial advantage some eight months ahead of the primary.

The reason for doubt is the track record of candidates running statewide following a previous statewide loss. The second time around has not shown much improvement in general election vote percentage (though each won their second round primaries, except for Neumann).

Name ID

Repeat candidates begin their second races with lower name ID than when they finished their first race, with slippage of about 20 points for Barrett and Feingold. Hovde began both races with very low name ID. All ended their second races with high name ID, though Feingold didn’t quite reach the high levels he had in 2010.

Barnes began his 2022 Senate race with a name ID rate in the mid-30s, rising to the mid-80s. We don’t yet know how much that has declined since 2022.

The chart shows the changes in name ID across the year leading up to each election. There is need to rebuild name recognition in the second act, but candidates largely succeed in doing so, and start with a higher level than first time candidates.

Net favorable ratings

Each of these candidates has suffered declines in net favorability across their elections. Decline late in the campaign is apparent for each candidate. Feingold stands out for having net positive favorability in both races he lost. The others all ended in negative territory, with Barrett and Hovde more net negative in their second races than in their first. Feingold’s first and second are about equal.

Bottom line

We don’t know how the next eight months until the primary, and eleven months to the general election, will unfold. What these past second acts have shown in that initial advantages in name ID and campaign experience, including established donors, have not produced success in the second campaigns over the past quarter of a century. Barnes now has the chance to change that somewhat daunting record.